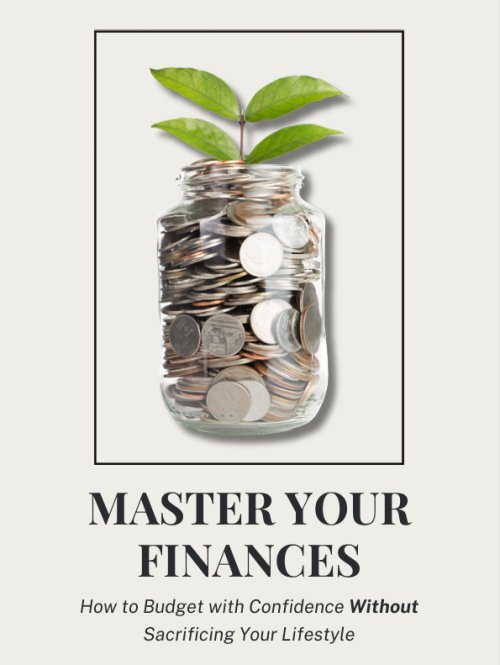

A Practical Guide To Side Hustles, Bill Cuts, And Year-End Tax Prep

Want calmer money months and a smoother April? We share practical side hustles, negotiation scripts, automation tips, and strategic year-end deductions. Hit play, then share the one tactic you’ll try today. Which strategy grabbed you most?

Most money wins start small. Learn how to launch a side hustle, cut sneaky bills, automate savings, and close the year with smart tax moves. Ready to keep more of what you earn? Listen now and tell us your next step! What will you tackle first?

Small money moves rarely make headlines, yet they quietly change bank accounts. That’s the core idea running through our talk: build income with skills you already have, plug the leaks hiding in your recurring costs, and automate good behavior so progress keeps rolling even when life gets busy. We began with a mindset reset. Improving your finances doesn’t need a dramatic leap or a perfect plan. It needs one practical action you can start this week. Treat your time with intention, track outcomes, and choose tools that reduce friction. The compounding effect of consistent, small actions turns into visible results over months, not minutes.

We push for a simple path to more income: start a small, focused side hustle based on one marketable skill. The trick is to act like an owner from day one. Set work hours, define a clear offer, and use marketplaces like Upwork or Fiverr to find your first clients fast. Track every dollar to see what works. In parallel, invest in upskilling. Pick a high-demand skill in your industry such as data analysis, project management, or digital marketing, then build a mini portfolio. Create a sample campaign, dashboard, or project plan that proves capability. Portfolios open doors because they convert claims into evidence.

Cutting costs is not about deprivation, it’s precision. Start with a subscription audit and list every monthly and annual charge. Cancel what you don’t use and negotiate the essentials. A short, polite script paired with competitor pricing often lowers internet, phone, and even insurance bills. The key is reassigning the savings instantly. Move them to a high-yield savings account, or buy a tool that upgrades your earning ability. Automation then locks in your gains. Schedule transfers the day after payday to build an emergency fund and feed a low-cost investment account. You never see the cash, so you never miss it, and consistency does the heavy lifting.

To avoid overwhelm, we laid out a four-week plan. Week one: audit and negotiate. Week two: automate saving and investing. Week three: launch the side hustle or set up your service page. Week four: choose a skill to pursue and enroll in a focused course. Each step takes a small block of time but raises your financial baseline. After six to twelve months, you’ll likely see higher income, lower fixed costs, and a steady savings habit, all without upending your life. Progress beats perfection, and systems beat willpower.

We then shifted to year-end tax planning, where organization, timing, and documentation can trim your tax bill and reduce stress. Start by reconciling your books and backing up digital records. Gather W-2s, 1099s, 1098s, brokerage statements, property tax receipts, and bank statements. For charitable giving, ensure donations clear by December 31 and keep proper acknowledgments. Consider bunching multiple years of donations to exceed the standard deduction. Business owners should review ordinary and necessary expenses, track a contemporaneous mileage log, assess home office eligibility, and evaluate equipment purchases that qualify for Section 179 or bonus depreciation.

Beyond charity and business deductions, scan for medical expenses thresholds, education costs, student loan interest, SALT limits, and energy-efficient home credits. Follow a simple timeline: early December for reconciliation and identifying deductible expenses to accelerate, mid-December to execute charitable gifts and payroll updates, late December for final purchases or prepayments where sensible, and early January to gather incoming forms. Keep receipts, logs, and acknowledgments tidy, and avoid aggressive positions without support. If you face complex choices, a qualified tax professional can save more than they cost. With clear records and a few timely actions, April becomes much calmer and your financial flywheel keeps turning.

Ready to build steady gains and a calmer tax season? Follow the plan, subscribe for more practical money tips, and leave a review to share what step you’ll take this week.

Purchase our Budgeting Workbook and Monthly Budget spreadsheet and get a head of the tax game before the end of the year. For a limited time the price is just $20. Get it fast and easy! Download it Now!

When you advertise on Income Talk Podcast, you are maximizing your potential to reach a mass audience. Every mention, Every Ad Spot is heard. What are you waiting for?

Share

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

1

Love

1

Funny

0

Funny

0

Angry

0

Angry

0

Sad

0

Sad

0

Wow

0

Wow

0